Why Your Best Team Might Be Building Your Worst Disaster

Picture this: A talented leadership team. Top-tier credentials. Flawless execution. Every metric trending green. And yet, five years later, the company is fighting for survival—or worse, gone entirely.

This isn’t a story about incompetence. It’s something far more insidious. It’s about intelligent people trapped inside a system that rewards them for making precisely the wrong choices.

The Athletic Metaphor That Explains Everything

Want to see this pattern in pure form? Look at how different sports organizations develop talent.

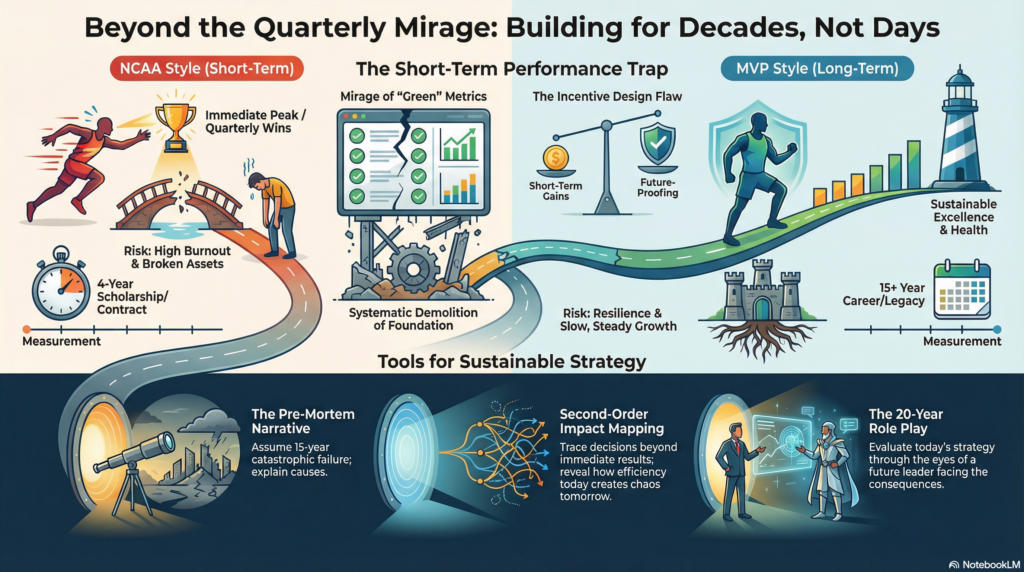

Jamaica’s MVP Track Club has produced Olympic champions and world record holders whose careers span decades. Athletes like Shelly-Ann Fraser-Pryce and Elaine Thompson-Herah didn’t just win races—they sustained excellence well into their thirties, their bodies intact, their bank accounts healthy.

Meanwhile, the American collegiate athletics system—the NCAA—operates like a different species entirely. Talented high schoolers arrive with Olympic potential. Four years later, many flame out, never to compete internationally again. Bodies broken. Dreams abandoned.

Here’s what makes this fascinating: NCAA coaches aren’t incompetent. These are world-class professionals running billion-dollar programs with access to cutting-edge sports science. They track everything—times, splits, recovery metrics, nutrition, biomechanics.

Yet they’ve built a machine designed to extract maximum performance over four years, regardless of what happens afterward. The system optimizes perfectly—for conference championships, television contracts, recruitment rankings. And in the process, it systematically destroys the very athletes who make those outcomes possible.

MVP asked a different question entirely: What does success look like measured over a fifteen-year career instead of a four-year scholarship? The answer required sacrificing immediate gratification—forgoing certain meets, accepting slower progression, resisting the pressure to peak too early.

The NCAA doesn’t fail because its people are stupid. It fails because every incentive, every measurement, every reward structure points them toward short-term glory and long-term destruction. And every dashboard they monitor confirms they’re doing exactly what they’re supposed to do—right up until the athlete graduates broken.

Now here’s the uncomfortable question: Is your company running the NCAA playbook?

The Corporate Version of Athletic Destruction

Corporate history is littered with smart people making decisions that looked brilliant on every spreadsheet while quietly demolishing the foundation beneath them.

Consider the financial sector meltdowns of recent decades. Before the 2008 crisis, before Enron, before the savings and loan disasters of the 1980s, things looked spectacular. Quarterly earnings beat expectations. Risk models showed green lights. Executives earned accolades for innovative financial engineering.

The long-term destruction was being created from day one. Not by people too stupid to see it, but by systems designed never to look for it.

Why Intelligence Doesn’t Protect You

The trap works like this: The CEO who sacrifices this quarter’s numbers to protect next decade’s foundation doesn’t get applauded at the board meeting. They get questioned. Their judgment gets doubted. Their compensation takes a hit.

Meanwhile, the executive who delivers short-term wins—even by mortgaging the future—gets promoted, celebrated, interviewed by business publications.

This isn’t a failure of intelligence, discipline, or execution. It’s a design flaw in how success gets measured.

The answer isn’t working harder within the existing framework. It’s redesigning the framework itself. That requires confronting existential questions about what you’re actually optimizing for—and having the courage to challenge metrics that everyone agrees are “obviously” correct.

Three Techniques to Surface Hidden Disasters

Here are practical methods to force your leadership team to see beyond the quarterly mirage:

- The Pre-Mortem Exercise

Gather your strategy team. Give them one instruction: Assume your current initiative has failed catastrophically fifteen years from now. Write the detailed story of exactly how and why.

Not vague organizational hand-wringing like “we didn’t execute well enough.” A specific, uncomfortable narrative that traces the chain of consequences from today’s confident decision to tomorrow’s wreckage.

The discipline is in the specificity. “We lost market share” is useless. “We optimized our pricing algorithm for immediate margin expansion, which slowly trained our best customers to view us as a commodity, which eroded pricing power, which forced us into a desperate discount spiral that destroyed brand equity and made us vulnerable to a well-funded competitor who simply waited us out” is useful.

- The Second-Order Impact Map

Most strategy discussions evaluate immediate effects and stop there. “This restructuring reduces overhead by 18%.” Applause. Meeting adjourned.

The second-order map refuses to stop. It forces the room to keep pulling the thread: That cost reduction eliminates redundancy. Which reduces organizational resilience. Which means the next market shock hits harder. Which forces emergency measures. Which creates exactly the kind of chaos that drives your best people to competitors. Who use them to build what you should have built.

Keep pulling until the consequences become uncomfortable enough to reconsider the decision.

- The Twenty-Years-Later Role Play

Identify the youngest person in your leadership team. They become a time traveler.

It’s twenty years in the future. A new generation of leaders asks them: “What was it like in that 2026 strategy session? What did your team decide?”

They respond with two scenarios. First, the courage scenario: “We confronted the hardest questions. We acknowledged uncomfortable truths. We made decisions that hurt short-term but protected long-term. Here’s how it played out.”

Second, the cowardice scenario: “We pretended things we knew weren’t true. We optimized for looking good rather than being good. We told ourselves comfortable lies. Here’s the price we paid.”

The technique works because it makes abstract future consequences feel visceral and immediate.

The Choice That Defines Leadership

Every organization faces the same fundamental question: Are you building an MVP or running an NCAA program?

Are you optimizing for sustainable excellence or spectacular quarterly performance? Are you protecting the foundation or mining it for short-term gains?

The smartest people in the room will keep making the worst decisions until the room itself gets redesigned. Until the metrics change. Until the incentives shift. Until the questions being asked force long-term consequences into immediate view.

The techniques exist. The choice is whether you have the courage to use them.

P.S. Five Prompts for Deeper Reflection

Use these with your preferred AI to explore how these patterns might be operating in your specific context:

- “I’m a [your role] at a [your industry] company. We’re currently optimizing for [your key metric]. Help me identify what long-term value we might be destroying in the process. Be brutally specific about the chain of consequences I’m not seeing.”

- “Run a pre-mortem analysis: It’s 2040, and the strategy we implemented in 2025 has failed catastrophically. Write the detailed story of how our decision to [your current initiative] led to our downfall. Don’t hold back on uncomfortable specifics.”

- “I need a second-order impact map. Our first-order effect from [your decision] is [immediate outcome]. Help me trace at least five levels deeper into the consequences, particularly the ones that would take years to surface but would be devastating when they do.”

- “Create a dialogue between my 2025 self and my 2045 self. The older version has lived through the consequences of [current strategic choice]. What would they tell me that I’m not willing to hear right now?”

- “Analyze my industry through the NCAA vs MVP lens. Who in my competitive landscape is running the short-term optimization playbook? Who’s building for decades? What specific metrics distinguish them? What would it cost me to switch approaches?”